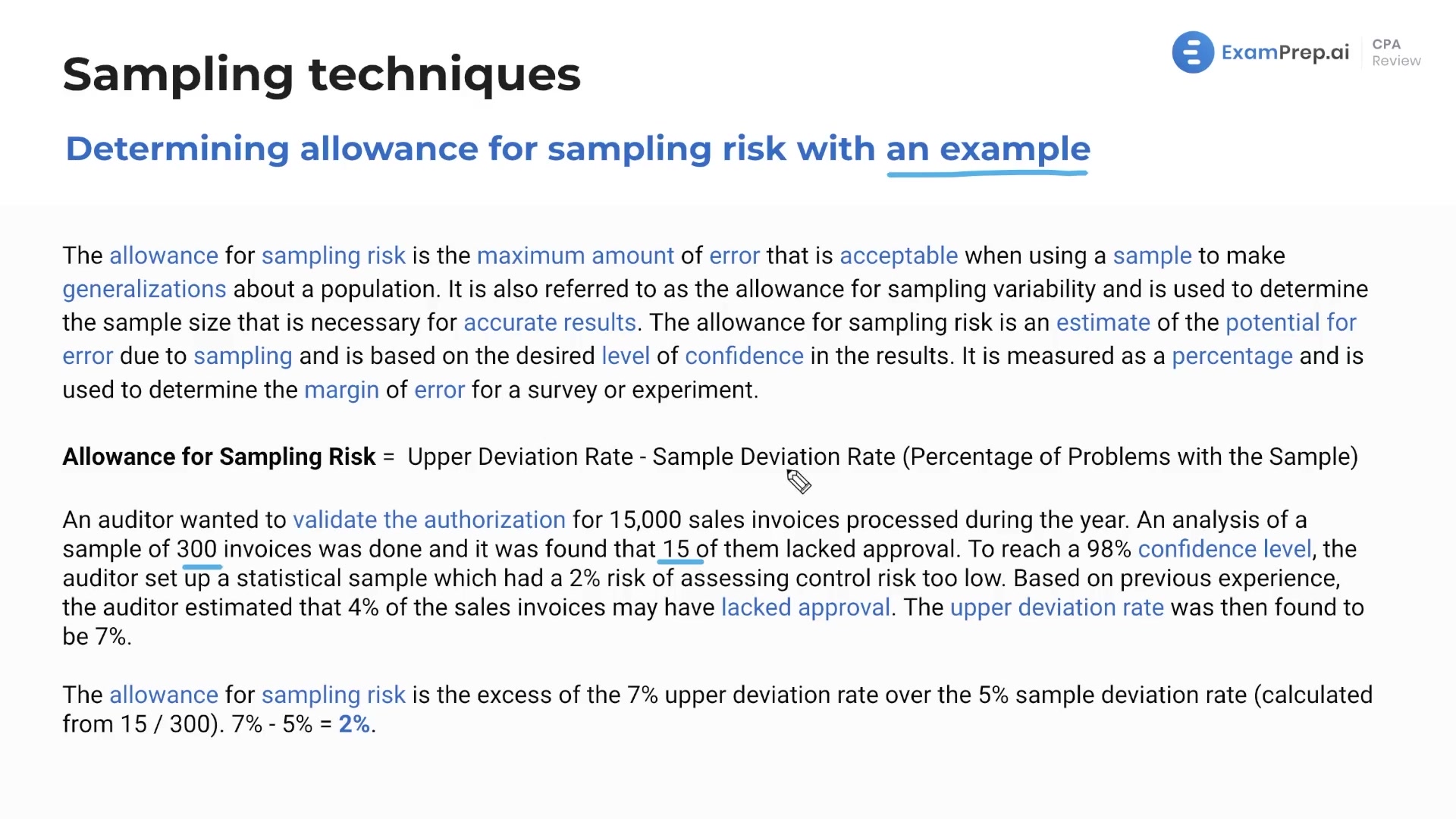

In this lesson, Nick Palazzolo explains the concept of allowance for sampling risk, which is the maximum amount of error acceptable when using a sample to make generalizations about a population. The lesson provides an example where an auditor validates the authorization for 15,000 sales invoices, with a sample of 300 invoices analyzed. By calculating the difference between the upper deviation rate (given in the example) and the sample deviation rate (based on the sample problems), Nick illustrates how to determine the allowance for sampling risk. This concept is essential for auditors when determining the accuracy of their audit testing on transactions and account balances.

This video and the rest on this topic are available with any paid plan.

See Pricing