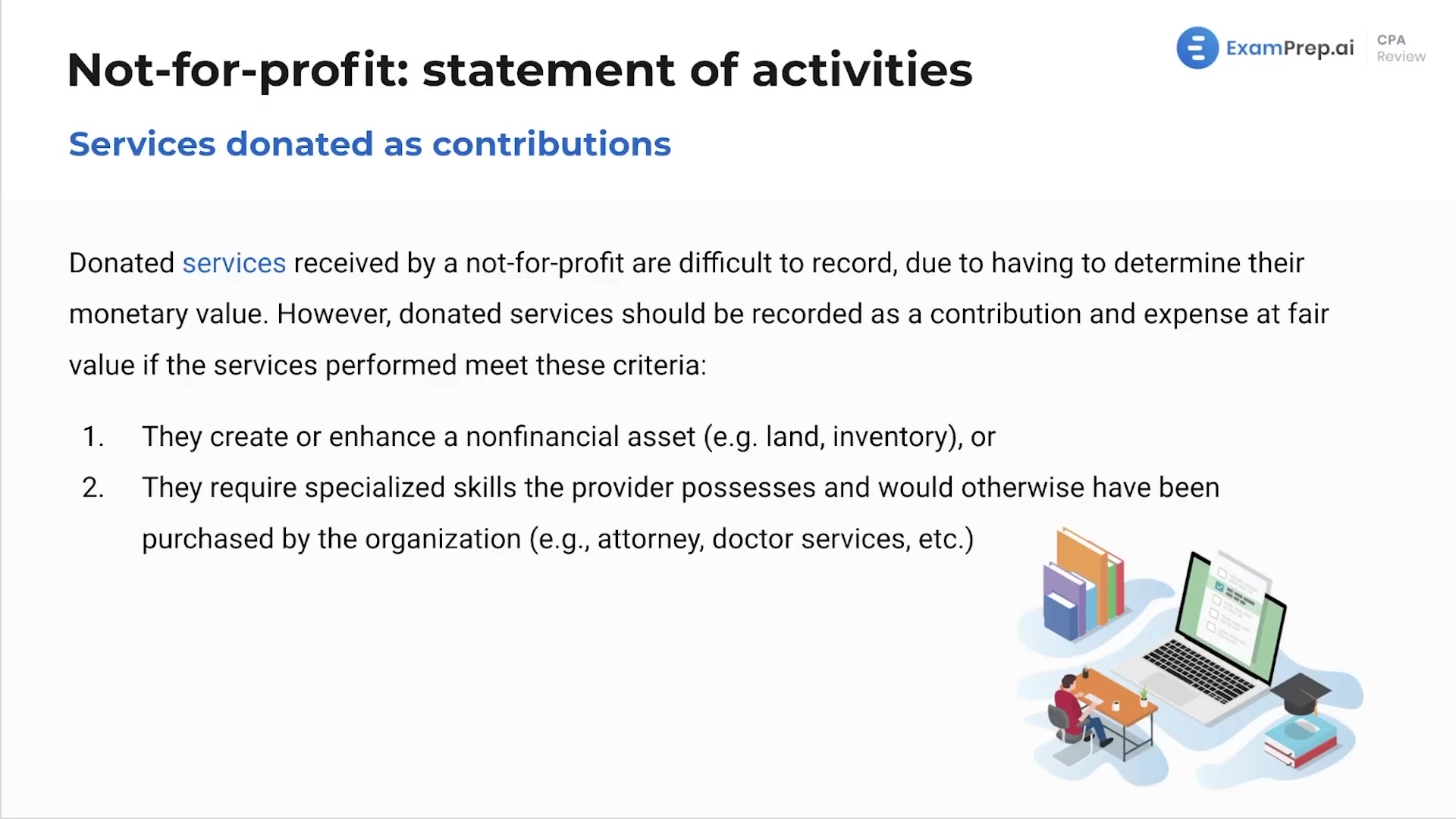

In this engaging lesson, Nick Palazzolo, CPA, breaks down the complexities of accounting for donated services received by not-for-profit organizations. He clarifies when and how to value these contributions, providing illustrative examples ranging from tax services to bricklaying and medical expertise. This discussion highlights the criteria for recognizing donated services as both contributions and expenses, focusing on the enhancement of non-financial assets and the use of specialized skills. Nick also explores common situations, such as lawyers offering pro bono services and physicians providing subsidized care, detailing how to record these at the appropriate market rates. Additionally, the lesson covers the practical application of these principles with the examination of pertinent journal entries.

This video and the rest on this topic are available with any paid plan.

See Pricing