Considerations Specific to Planning and Performing a SOC Engagement

Special considerations for planning and performing a Service Organization Control (SOC) engagement include assessing the service organization’s control environment, pinpointing the relevant trust service criteria, and determining the sufficiency of evidence to report on the effectiveness of the controls in place.

Lesson Videos

Considerations Specific to Planning and Performing a SOC Engagement - Overview

Considerations Specific to Planning and Performing a SOC Engagement - Overview

Introduction to Considerations Specific to Planning and Performing a SOC Engagement

Introduction to Considerations Specific to Planning and Performing a SOC Engagement

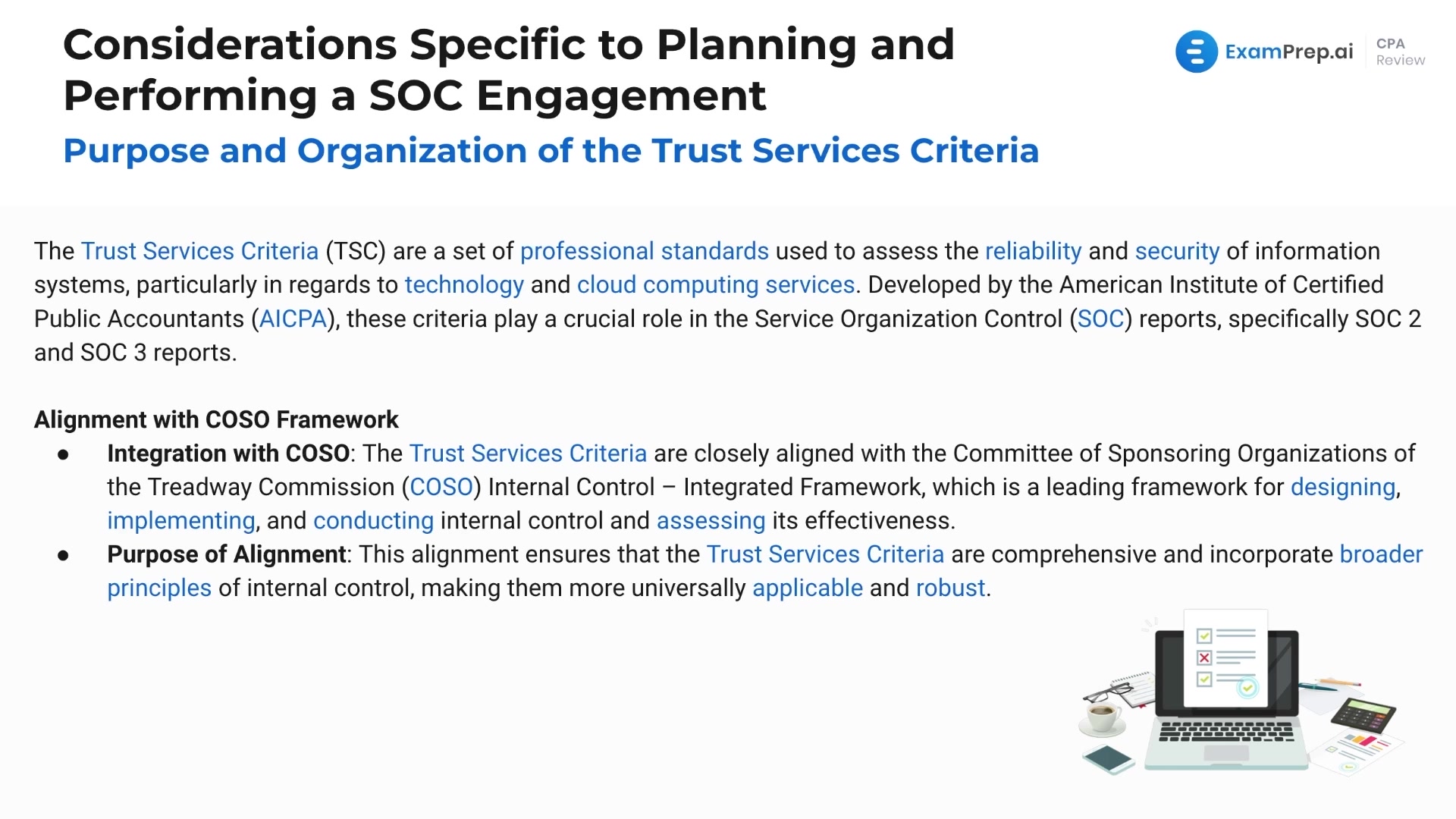

Purpose and Organization of the Trust Services Criteria

Purpose and Organization of the Trust Services Criteria

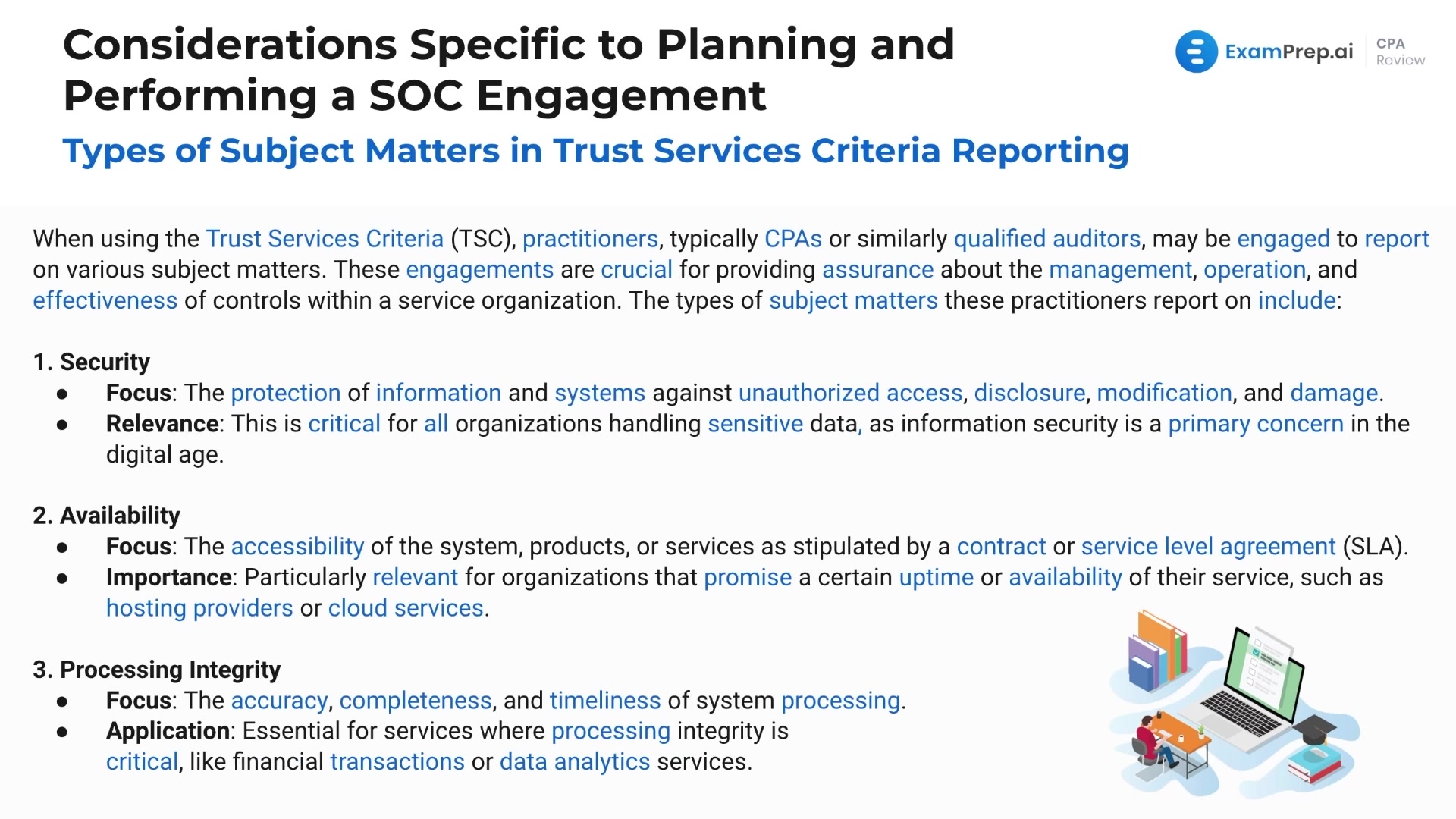

Subject Matters in Trust Services Criteria Reporting

Subject Matters in Trust Services Criteria Reporting

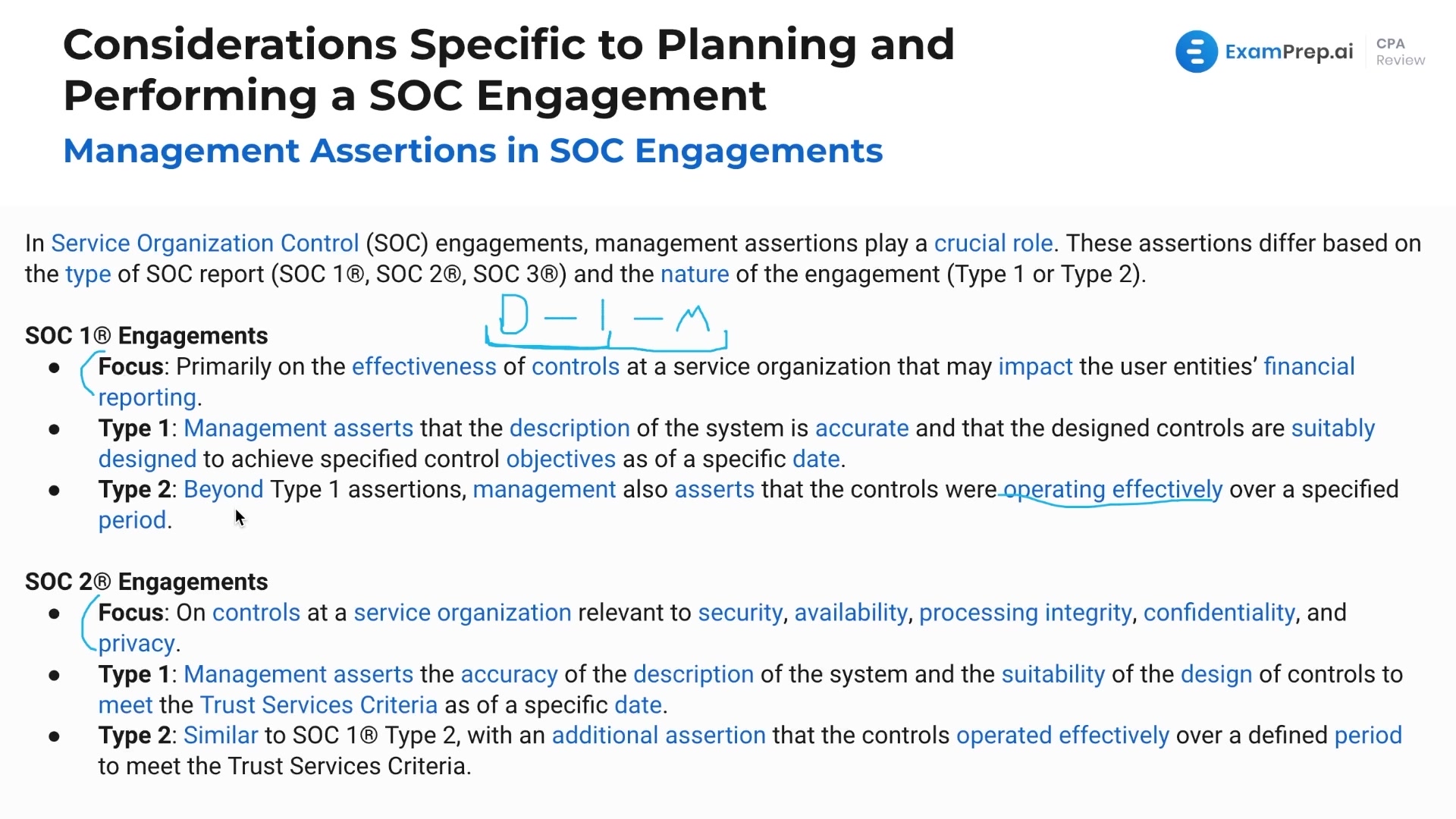

Management Assertions in SOC Engagements

Management Assertions in SOC Engagements

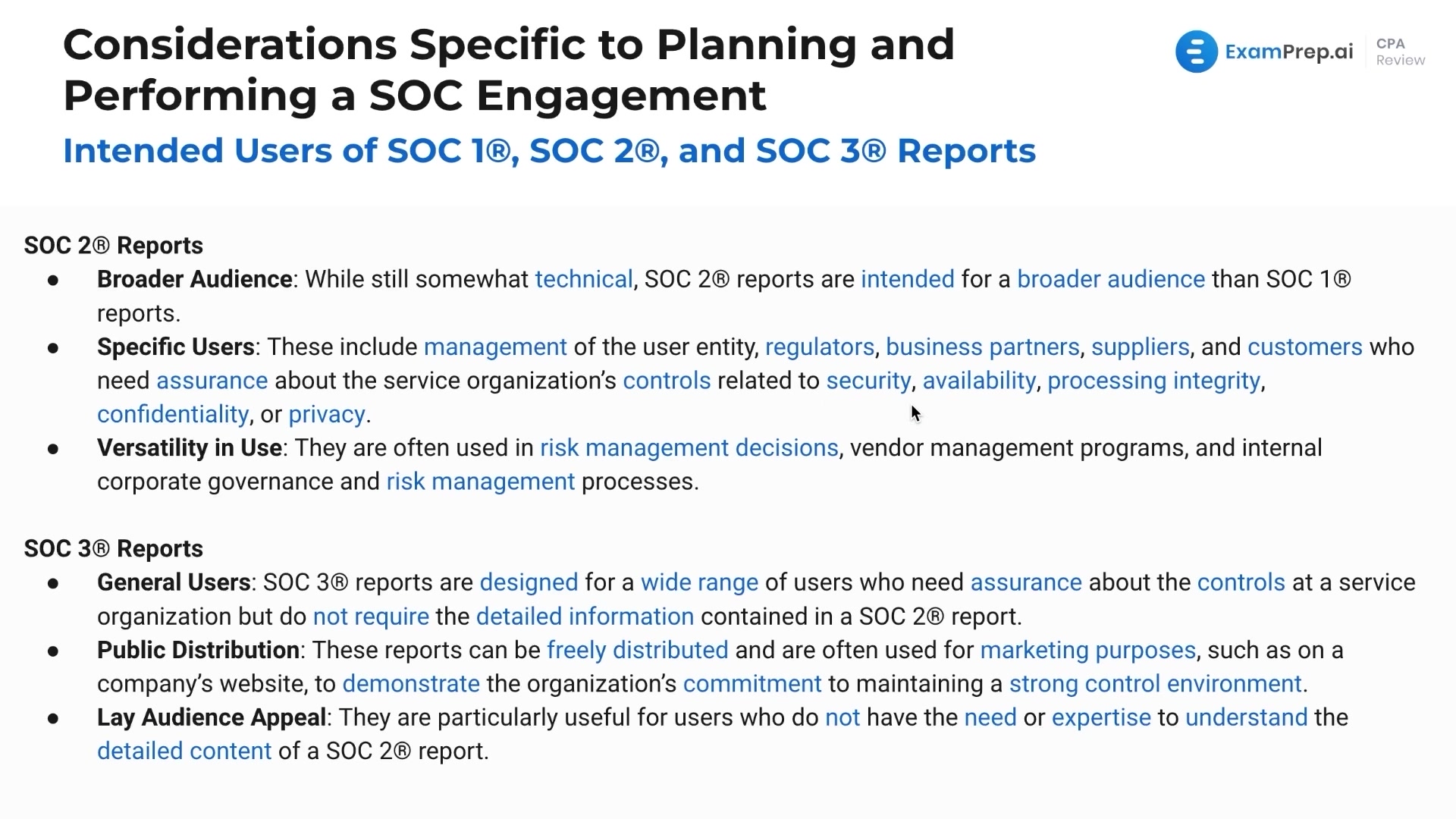

Intended Users of SOC 1, SOC 2, and SOC 3 Reports

Intended Users of SOC 1, SOC 2, and SOC 3 Reports

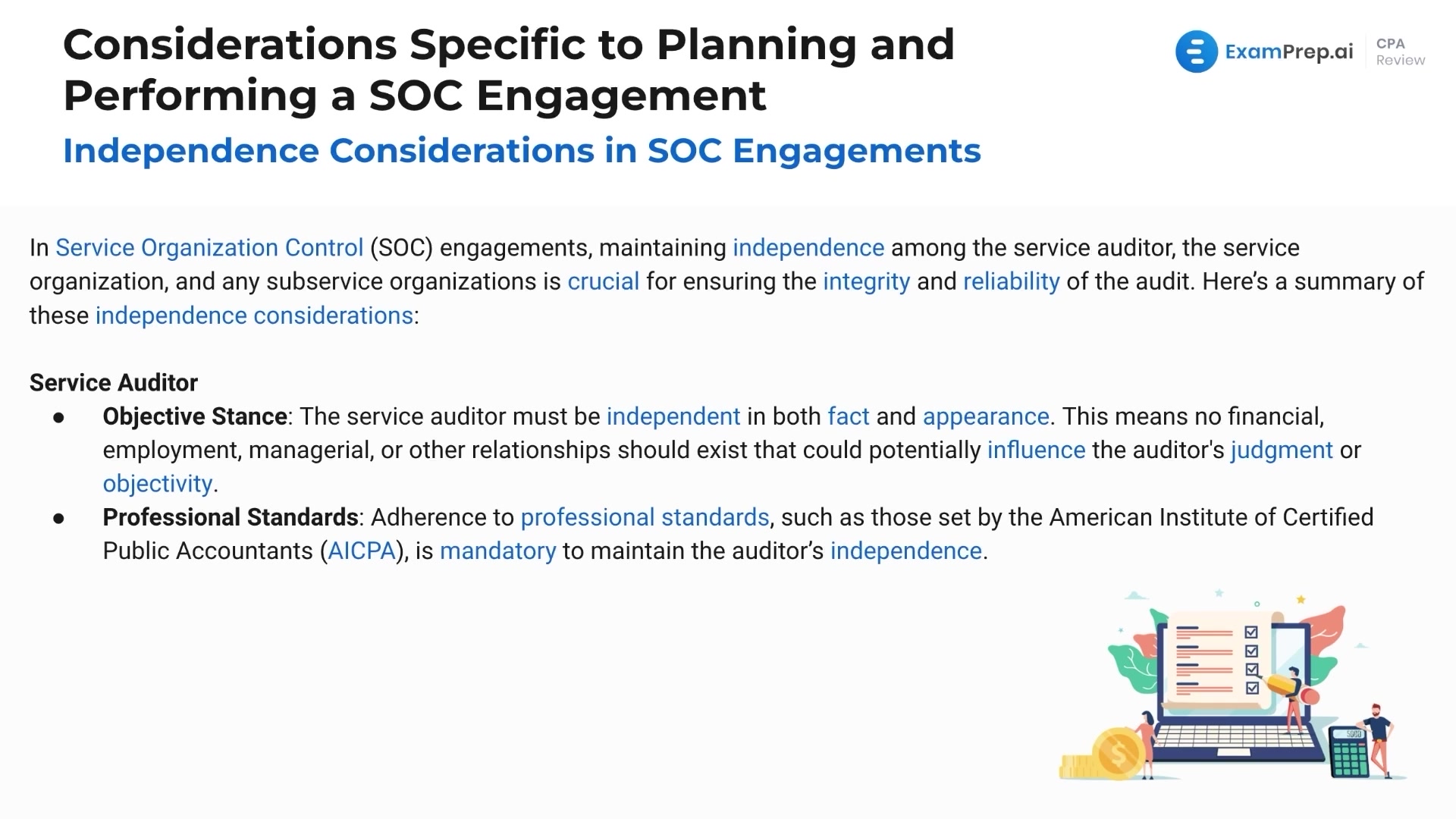

Independence Considerations in SOC Engagements

Independence Considerations in SOC Engagements

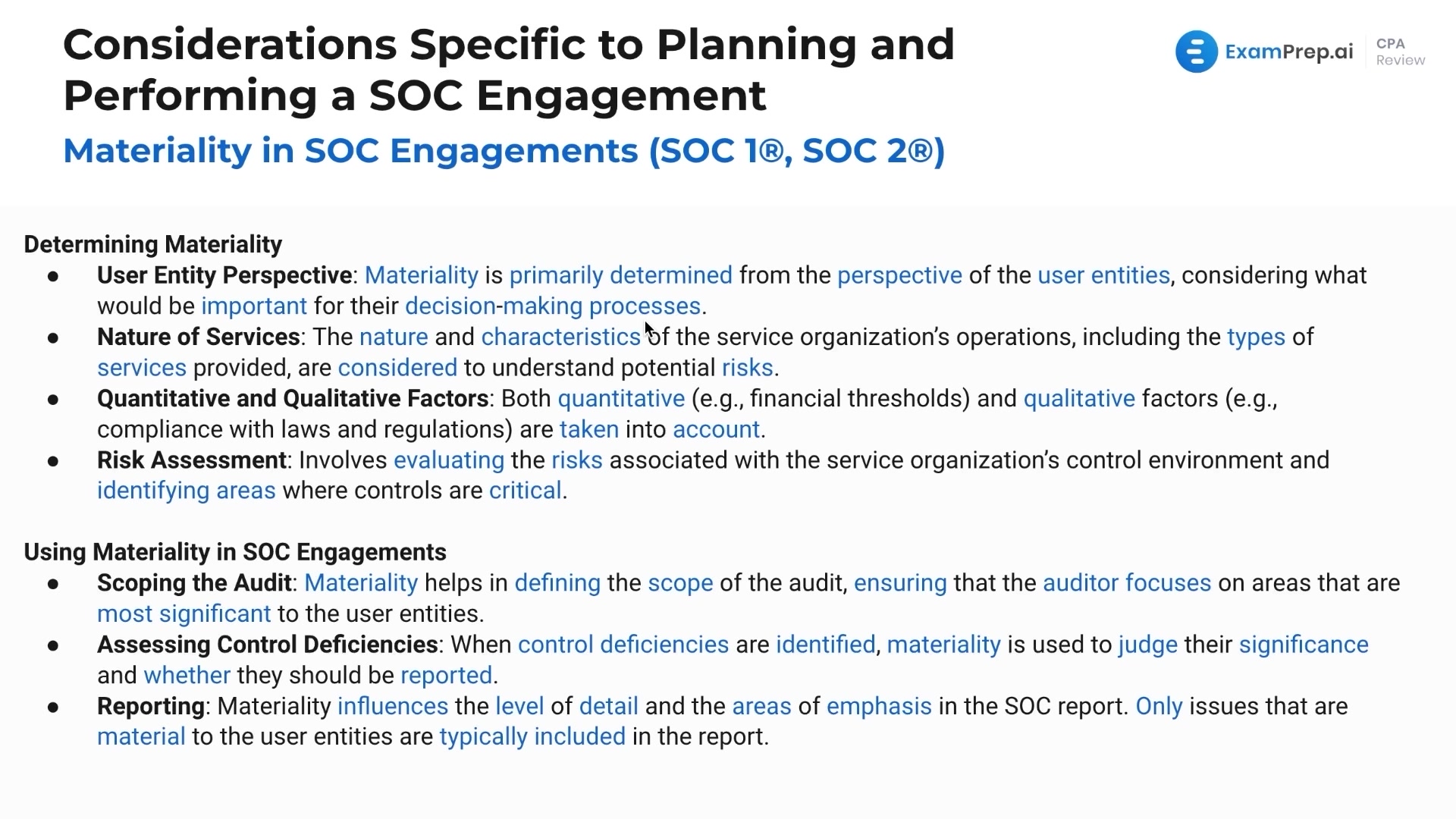

Materiality in SOC Engagements

Materiality in SOC Engagements

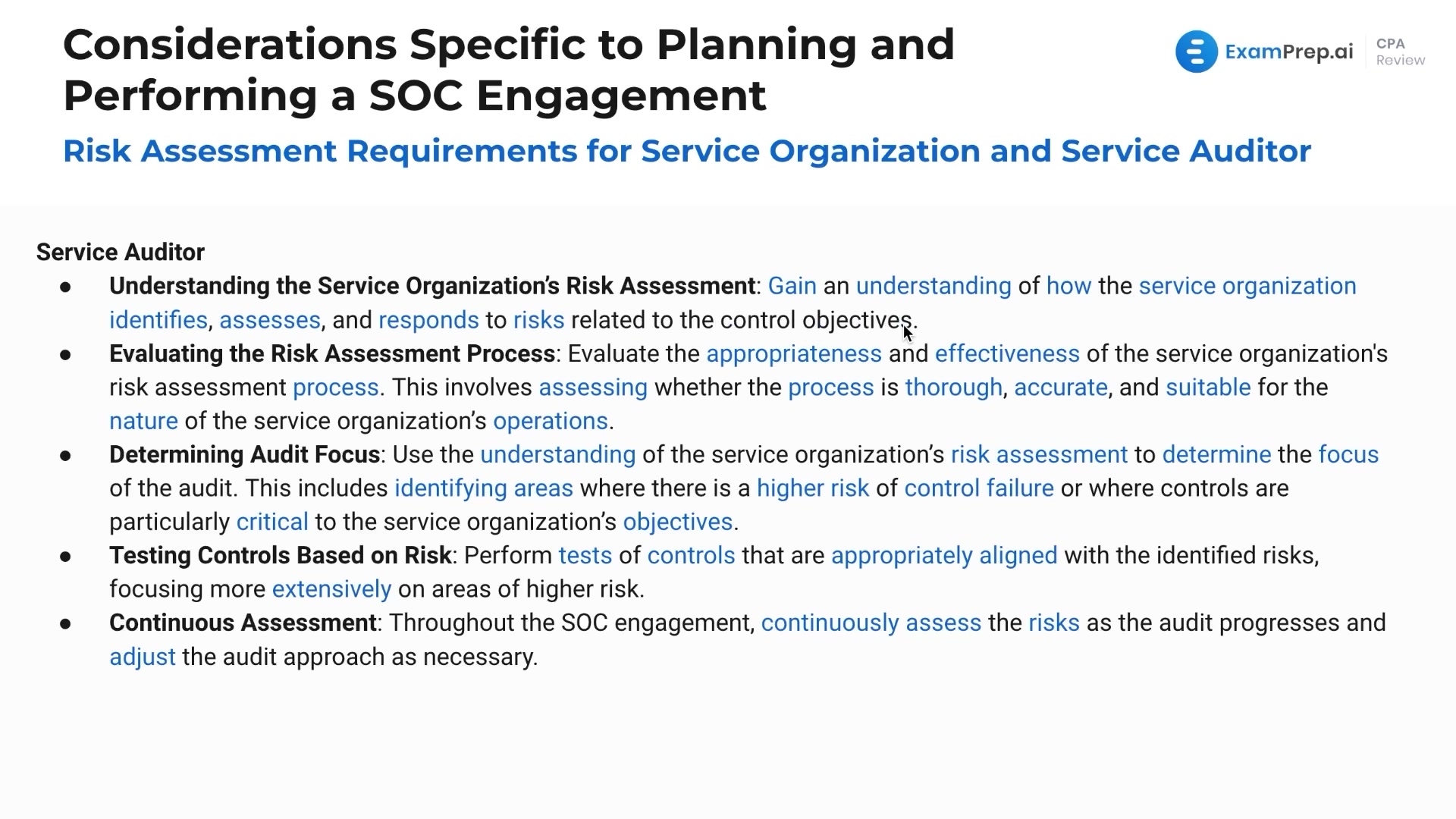

Risk Assessment for Service Organizations and Service Auditors

Risk Assessment for Service Organizations and Service Auditors

Criteria for a Vendor To Be Considered a Subservice Organization

Criteria for a Vendor To Be Considered a Subservice Organization

Inclusive v. Carve-out Method in SOC Engagements

Inclusive v. Carve-out Method in SOC Engagements

Service Commitments and System Requirements in SOC 2 Engagements

Service Commitments and System Requirements in SOC 2 Engagements

Subsequently Discovered Facts on SOC Engagements

Subsequently Discovered Facts on SOC Engagements

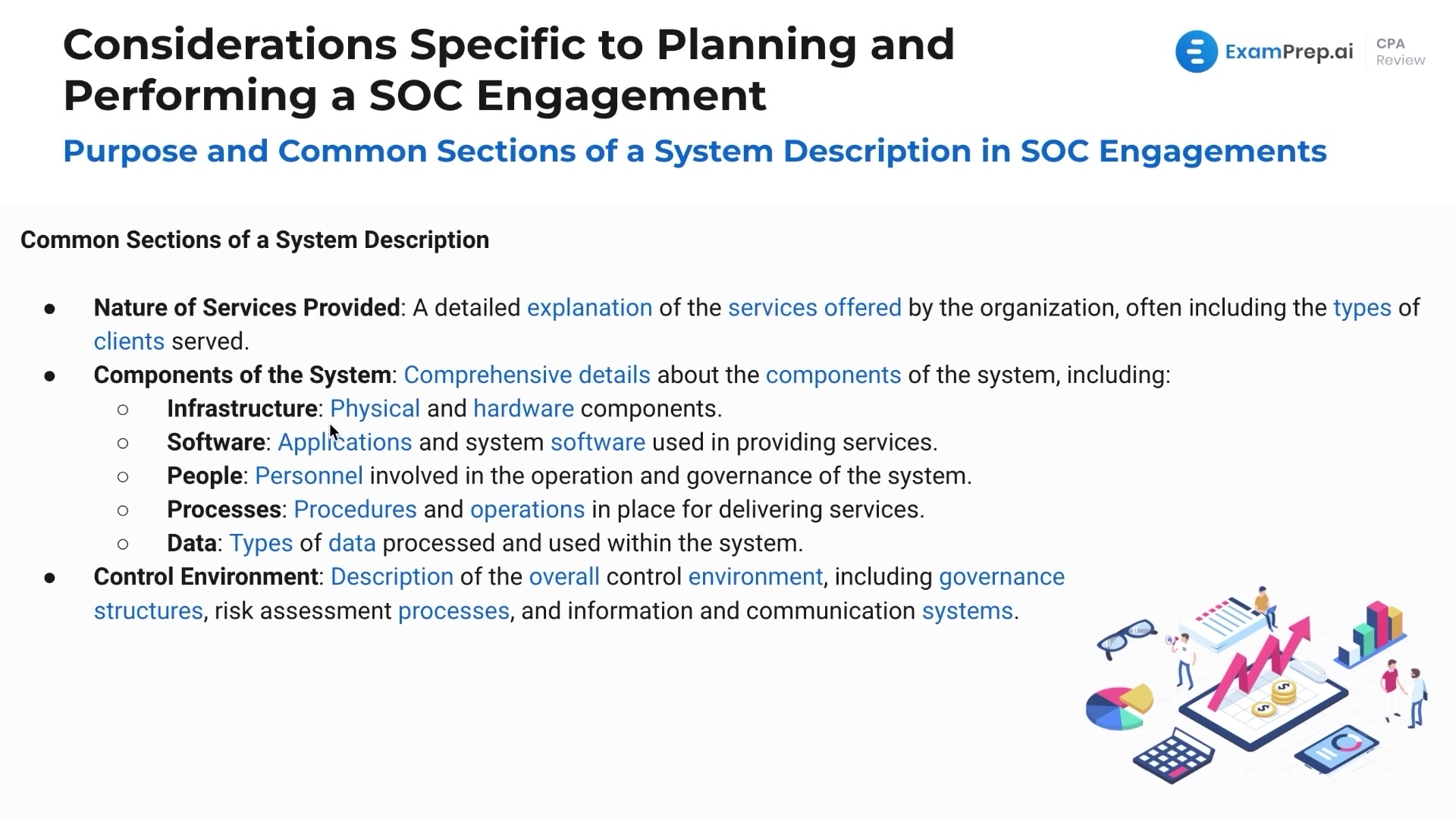

Purpose and Common Sections of a System Description in SOC Engagements

Purpose and Common Sections of a System Description in SOC Engagements

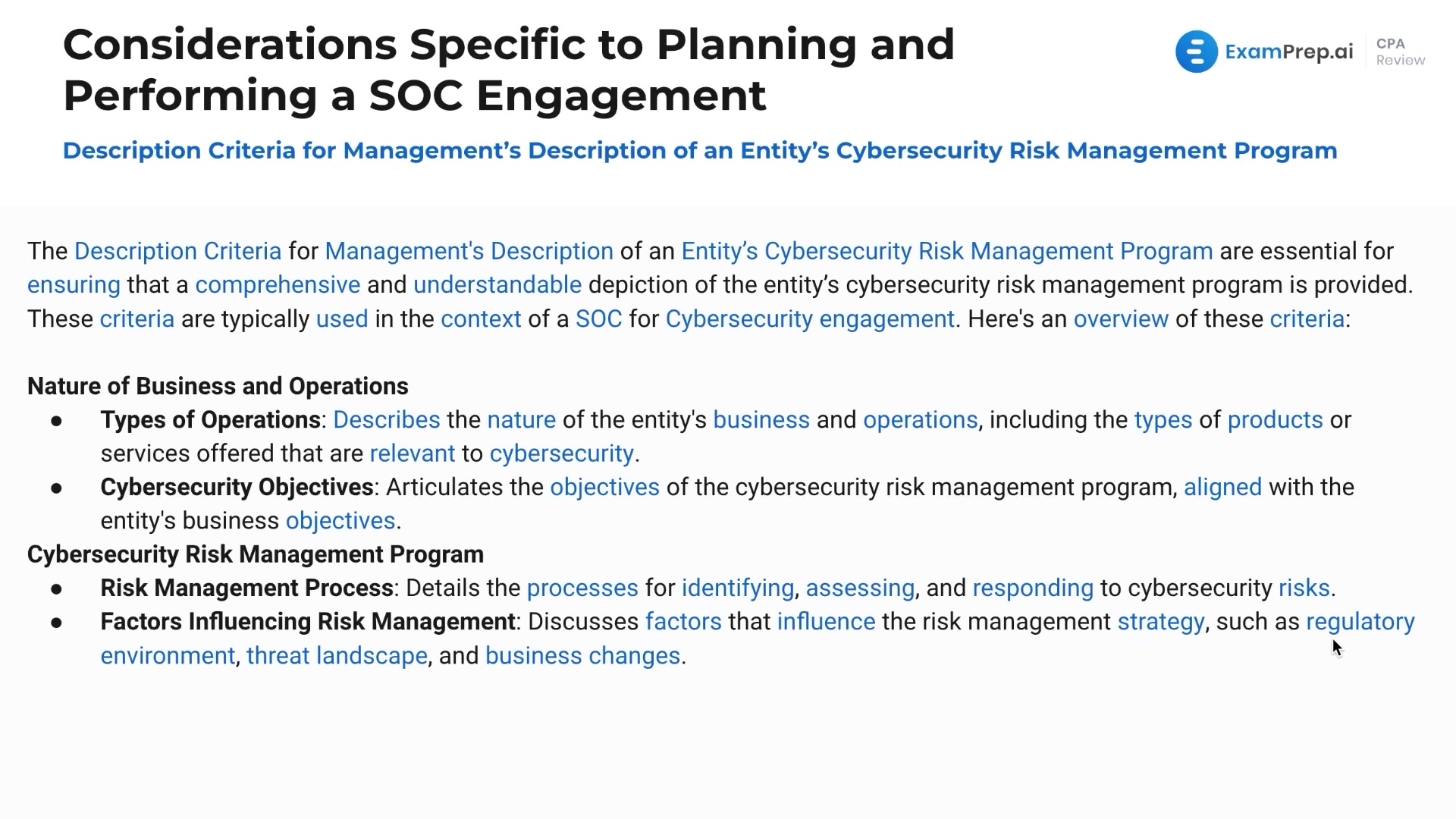

Management's Description of an Entity's Cybersecurity Risk Management Program

Management's Description of an Entity's Cybersecurity Risk Management Program

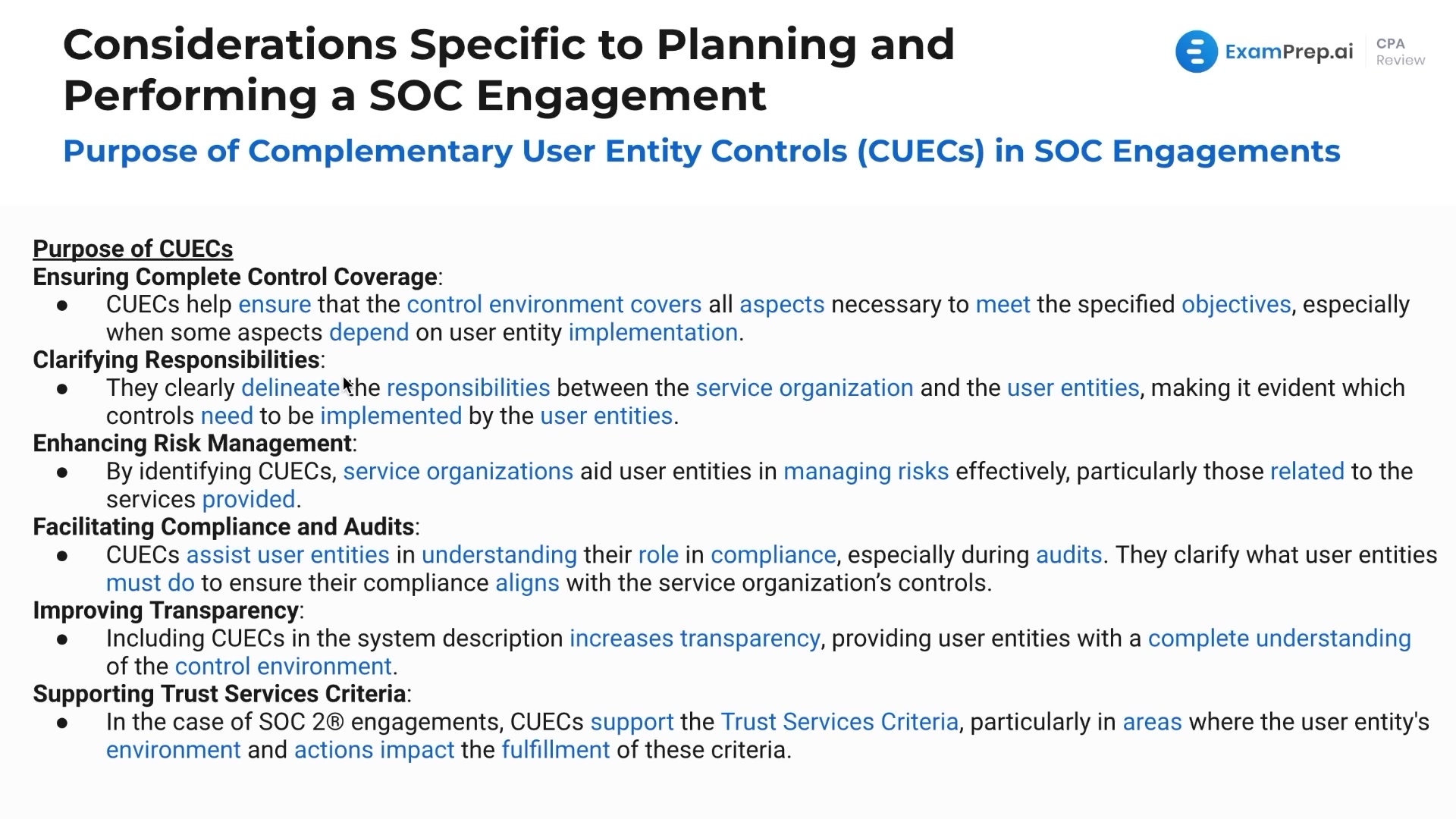

Complementary User Entity Controls

Complementary User Entity Controls

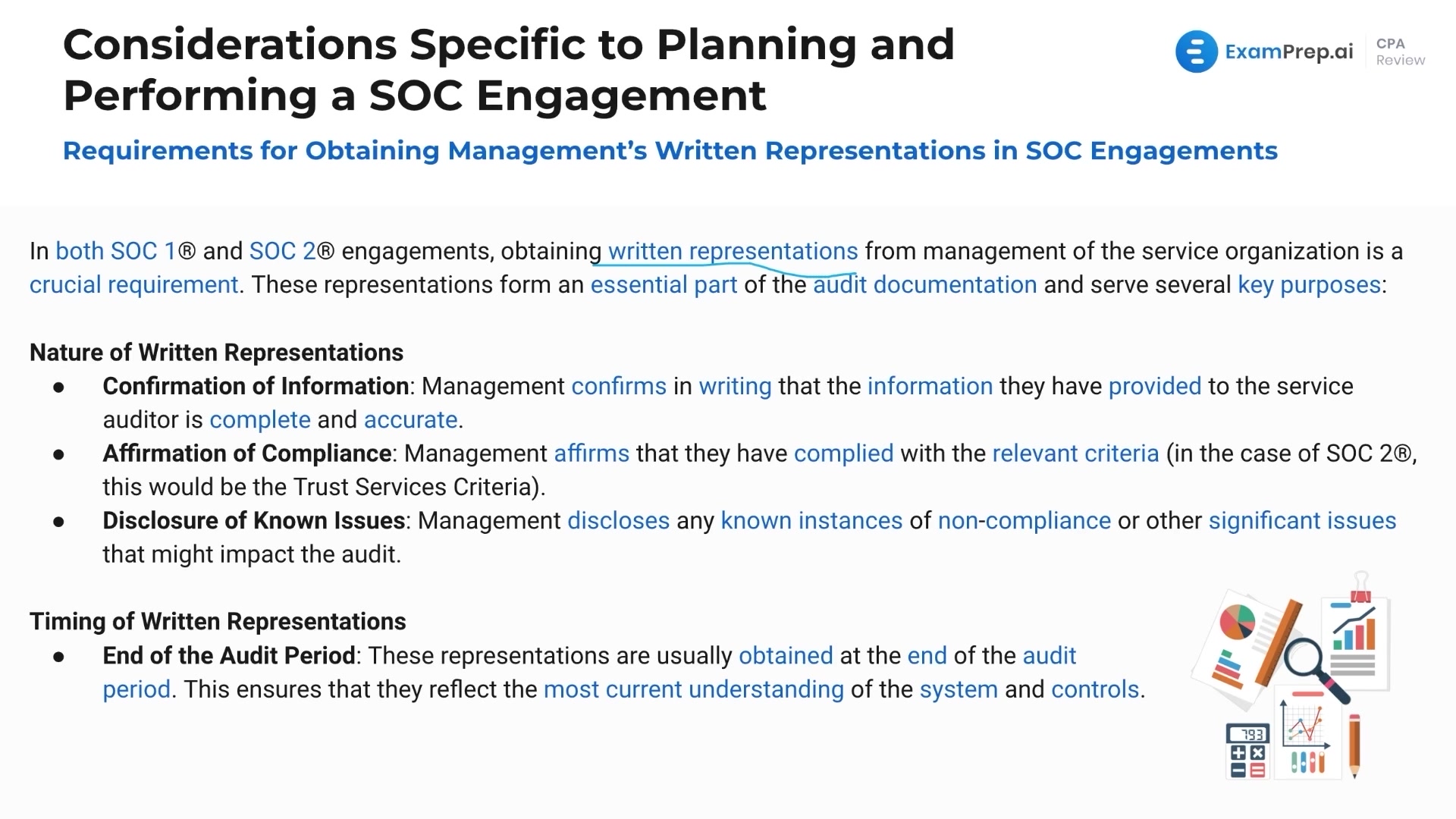

Obtaining Management's Written Representations

Obtaining Management's Written Representations

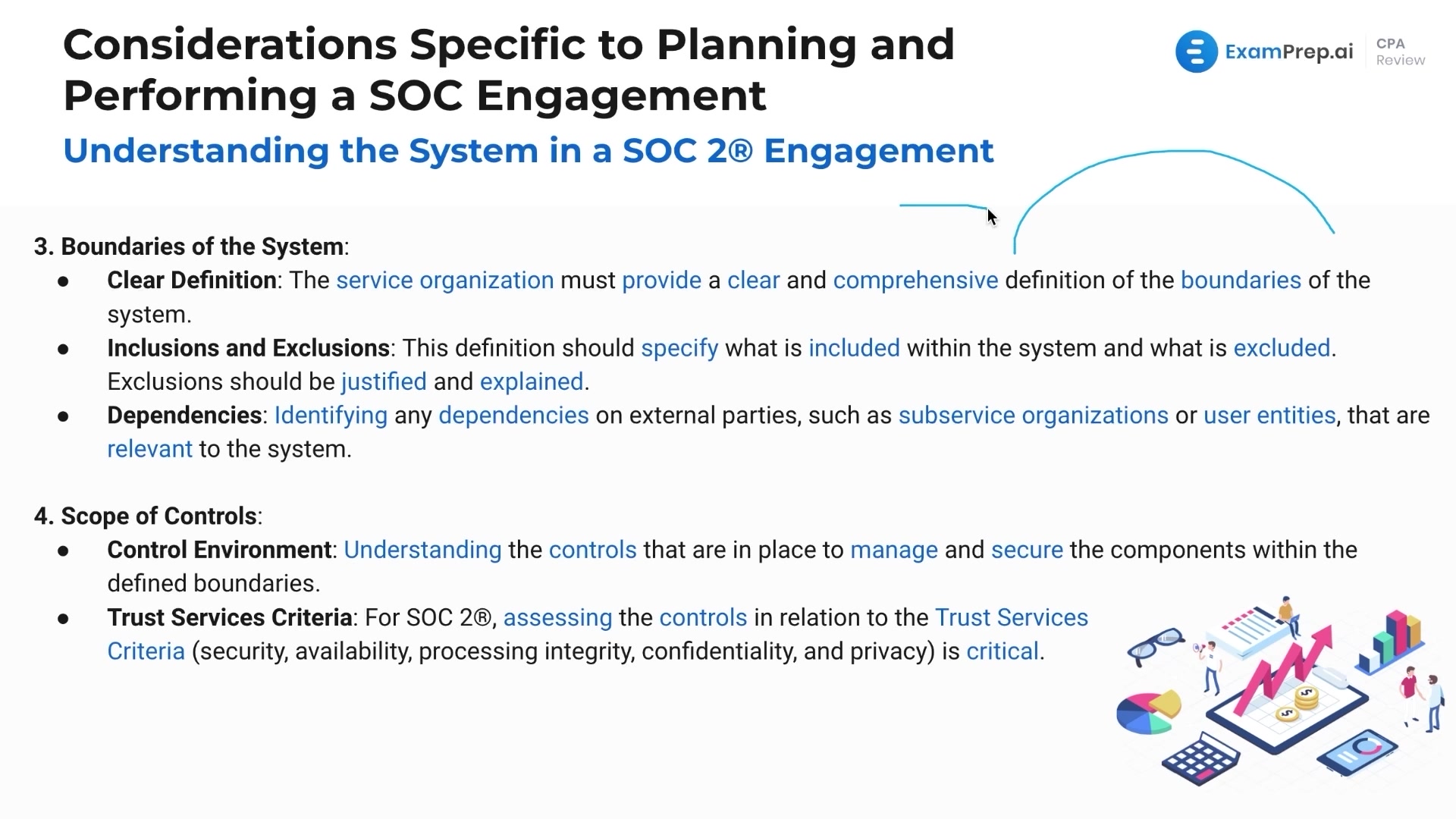

Understanding the System in a SOC 2 Engagement

Understanding the System in a SOC 2 Engagement

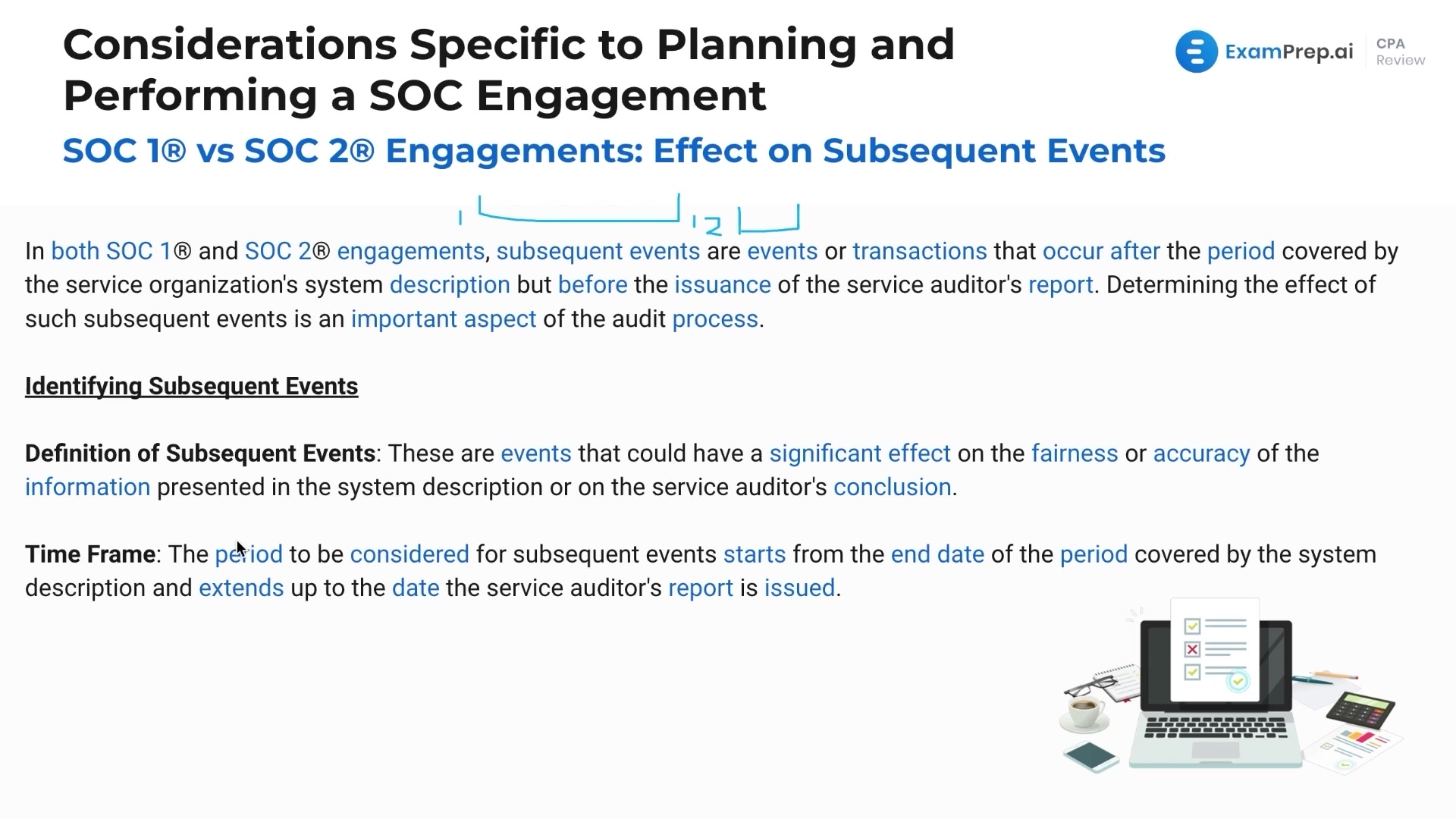

SOC 1 vs. SOC 2 Engagements

SOC 1 vs. SOC 2 Engagements

Considerations Specific to Planning and Performing a SOC Engagement - Summary

Considerations Specific to Planning and Performing a SOC Engagement - Summary

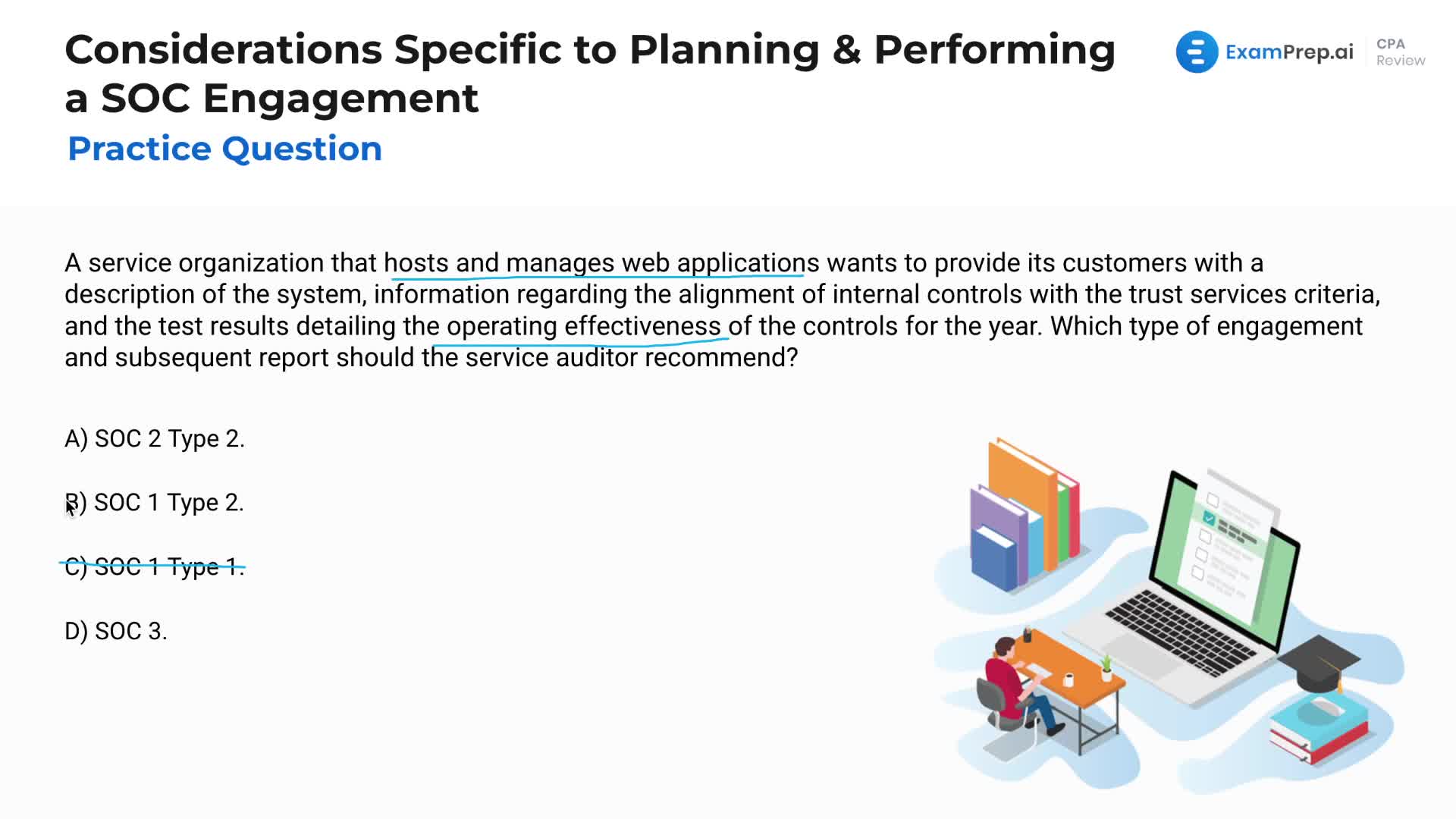

Considerations Specific to Planning and Performing a SOC Engagement - Practice Questions

Considerations Specific to Planning and Performing a SOC Engagement - Practice Questions

"Examprep.ai helped me pass all 4 CPA exams on the first try. I highly recommend. I especially like the feedback and ratings the software provides so I know where to focus my time."

Daniel H., CPA

"I can't recommend ExamPrep.ai enough. Nick's lessons turned concepts I struggled with into strengths. I was able to pass FAR right before other exams expired!"

Andrew K, CPA

"I just want to say thank you for the great lesson videos. I couldn't stay awake through lectures of another course. After watching all your FAR lessons I was finally able to pass!"

Alyssa M., CPA Candidate